Heqing SHI 施贺卿

Research

Working Papers 📖

- “Economics-Aware Machine Learning for Option-Implied Risk Metrics”

Coauthored with: Yi Cao, Zexun Chen

Presented at: EFMA 2025, ABFR Doctoral Symposium 2025

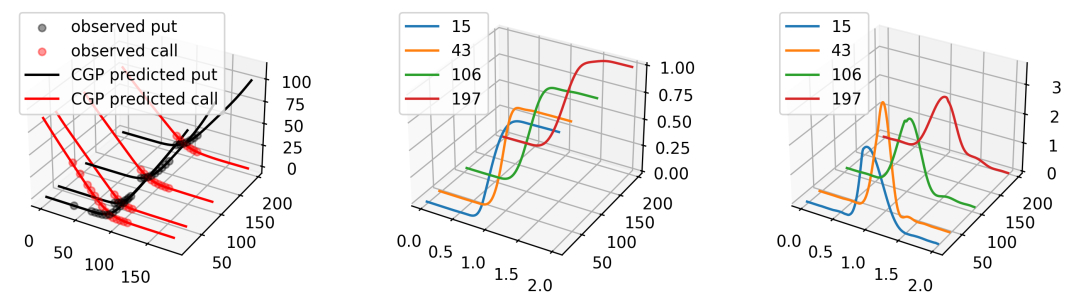

Abstract: The recovery (estimation) of asset return risk-neutral densities from cross-sectional option prices rely on strong model assumptions. At the same time, model-free recovery methods exist (see, e.g., Shimko (1993), Aït-Sahalia and Lo (2000), Figlewski (2010)), but they depend on the inter-/extra-polation of implied volatilities and the Black-Scholes formula. Both the model-based methods and the model-free methods work just fine for liquid, data-rich index options, but become brittle for illiquid, noisy stock options. We develop the Economics-Aware Gaussian Process which encodes the static no-arbitrage conditions ino the learned option price curves. Using the EAGP, we construct model-free stock-level RND aggregating both information from OTM call and put options. The EAGP-based RND improves the informativeness of a variety of metrics of stock returns, including the option-implied VaR, ES and moment-based metrics.

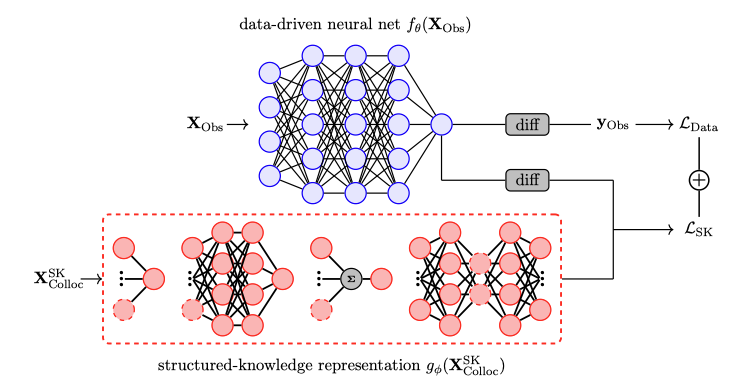

- “Bridging Structured Knowledge and Data: A Unified Framework with Finance Applications” [SSRN] [arXiv] [Video]

Coauthored with: Yi Cao, Zexun Chen, Lin William Cong, Guangyan Gan

Presented at: FoFI (Lancaster University Management School) 2026, ABFER 2026*, 中国金融科技学术年会 CFTRC 2026*, 42nd International Conference of the French Finance Association (AFFI), 5th Annual Hong Kong Conference on FinTech and AI in Finance, ESIF 2026*, SoFiE 2026*, EFMA 2026*, 2nd Frontiers in Finance Conference (中科大)*, 2026 金融未来学者论坛 Future Scholars in Finance Forum, 中国金融学术年会 CFRC 2026, CES 2026 China Conference, ESEM 2026†

Abstract: We develop Structured-Knowledge-Informed Neural Networks, a unified estimation framework that embeds theoretical, simulated, previously learned, or cross-domain insights as differentiable constraints within flexible neural function approximation. SKINNs jointly estimate neural network parameters and economically meaningful structural parameters in a single optimization problem, nesting approaches such as functional GMM, Bayesian updating, transfer learning, PINNs, and surrogate modeling. In an illustrative financial application to option pricing, SKINNs improve out-of-sample valuation and hedging performance, particularly at longer horizons and during high-volatility regimes, while recovering economically interpretable structural parameters with improved stability relative to conventional calibration. More broadly, SKINNs provide a general econometric framework for combining model-based reasoning with high-dimensional, data-driven estimation.

Publications 📕

† Conference to be presented.

* Conference presented by coauthor.