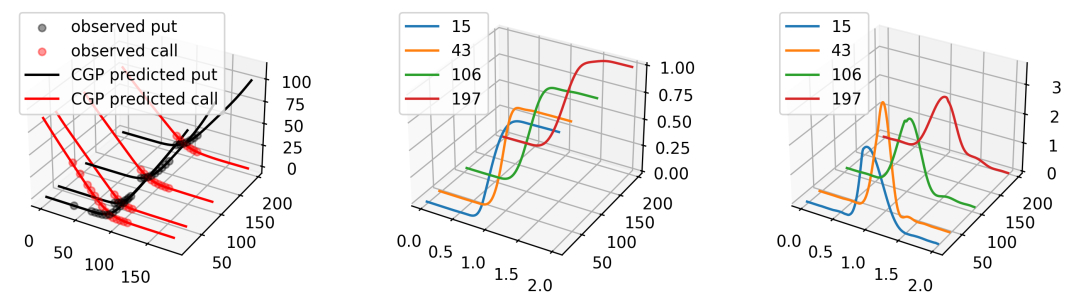

Model-Free Risk-Neutral Density with Constrained Gaussian Process:

I’m currently working on the estimation of predictive information for stocks from their options, together with my supervisors. We start from the Breeden and Litzenberger (1978) theorem and enhence the recovery of risk-neutral density (RND) by using a Gaussian process with constraints. The proposed constrained-GP RND-recovery method generates improved tail risk and moment estimations.

Example recovered RNDs for IBM

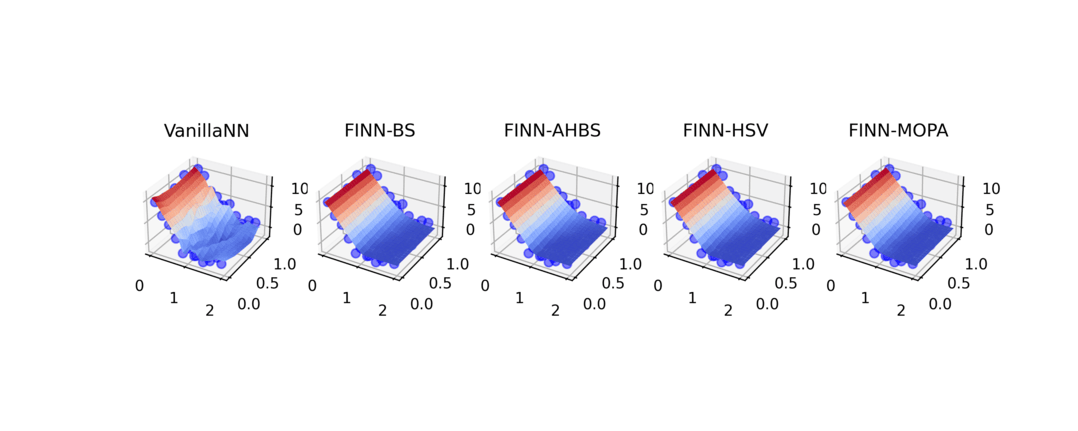

Finance-Informed Neural Networks for Option Pricing:

We propose a Finance-informed Neural Network (FINN) framework for option pricing which encodes the domain knowledge given by the functional of an option pricing model who admits a (semi) closed-form solution into a data-driven neural network. Our FINN framwork allows a battery of option pricing functionals, and outperforms both the plain data-driven neural network, and the structural models, for the tasks of pricing and hedging.

FINNs with various functional specifications with domain knowledge